February 2026 was no ordinary winter month on the Czech mortgage market. According to ČBA Hypomonitor data, it ranks among the five historically strongest mortgage months on record — and the numbers behind this result deserve a sober reading. Not to fuel euphoria, but because understanding the market correctly is the foundation of every sound investment decision.

Key figures for February 2026

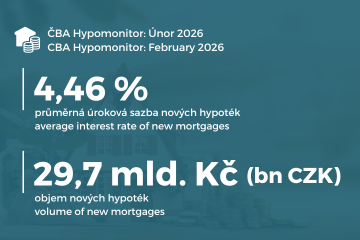

- New mortgage volume (excluding refinancing): CZK 29.7 billion. A 10% increase month-on-month; since the start of the year, new mortgage volume has reached CZK 56.7 billion — CZK 17 billion more than in the same period last year.

- Total mortgage market volume, including refinancing: CZK 40.5 billion. Refinancing and top-ups accounted for more than a quarter of the market, indicating that a significant share of clients are actively renegotiating the terms of their existing loans.

- Average interest rate on new mortgages: 4.46%. A slight decline from January’s 4.48%. Year-on-year, rates have fallen by just under 0.3 percentage points.

- Average new mortgage size: CZK 4.63 million. A 16% year-on-year increase, equivalent to CZK 630,000 more than a year ago. It is becoming increasingly evident that a wait-and-see approach to property purchases does not pay off in an environment of rising real estate prices.

In short: rates edged down, while households are taking out significantly larger mortgages.

Why such a boom — and why it is partly temporary

February’s figures cannot be read as the establishment of a new normal. Three factors converged simultaneously: a moderate decline in interest rates, continued growth in real wages, and — most notably — the approaching tightening of Czech National Bank conditions for so-called investment mortgages.

From April 2026, the Czech National Bank is recommending an LTV limit of 70% for mortgages on investment residential properties (down from the current 80%), along with a debt-to-income ratio (DTI) cap of seven times annual income. As a result, a portion of investors and individuals with investment motivations are rushing to secure financing under the current, more favorable conditions. February’s figures therefore partly reflect a shift of future demand forward — a stockpiling effect ahead of the April deadline.

What this means for the property market

The forces driving the current boom will not dissipate in April. Residential property prices have continued to rise in recent quarters, with price growth in several segments outpacing household income growth. Supplying new construction has chronically lagged demand. The tightening of investment mortgage conditions will naturally constrain some smaller individual investors who buy flats as buy-to-let assets. Demand for rental housing, however, will not disappear — it will simply shift, in part, from individual landlords to professionally managed portfolios. This is a trend already well established across Western Europe. The Czech Republic is only beginning to catch up.

Salutem Group: stable income where affordable mortgages end

The Salutem Group model operates on a different logic than the classic individual mortgage investment — and in the environment described by the February Hypomonitor, that logic is clearer than ever.

Salutem operates a model in which the investor acquires the property and Salutem then takes responsibility for its long-term letting and management. For the investor, this means stable rental cash flow that is not directly tied to the refinancing cycle of any single mortgage. Interest rate risk is managed not at the level of one contract, but across the entire portfolio — with the flexibility to work with varying fixed-rate periods and financing structures over time.

The February Hypomonitor is not an argument for overheated optimism, nor for retreating from real estate. It confirms that the Czech residential market remains active, while also entering a phase where outcomes are determined more than ever by the quality of the model, the location, and operational discipline — not merely by the level of interest rates. In such an environment, a well-structured model of secured rental income holds greater value than a bet on market timing.