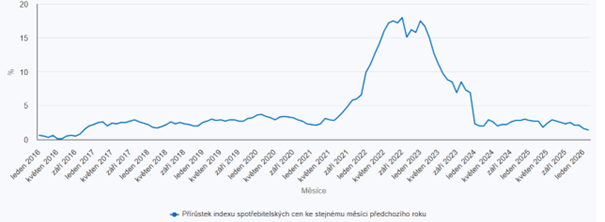

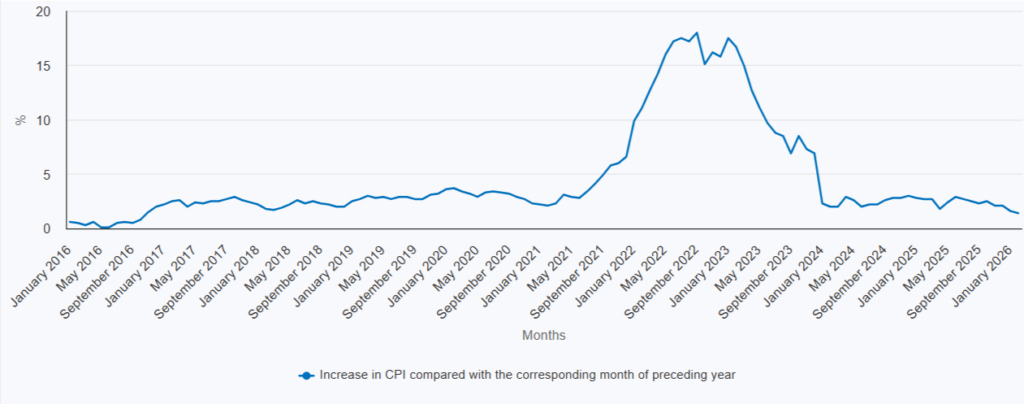

On Tuesday, 10 March 2026, the Czech Statistical Office released inflation data for February 2026. Year-on year inflation slowed to 1.4% in February 2026, marking a further decline from January’s 1.6%, driven primarily by slower growth in the prices of food, non-alcoholic and alcoholic beverages, and tobacco. On a month-on-month basis, consumer prices even edged down by 0.1%.

- Annual inflation: 1.4% (down from 1.6% in January).

- Core inflation remained unchanged at 2.7%

- Month-on-month change: -0.1%.

- Goods prices fell by 0.7% year-on-year, while services prices rose by 4.5%. Services therefore remain the main source of persistent inflation.

- HICP (European comparison): Under the HICP methodology, inflation in the Czech Republic stood at 0.9% in February. The Czech Republic matched Cyprus, which recorded the lowest rate within the euro area. For comparison, the estimated euro area average was 1.9%, Germany stood at 2.0%, and Slovakia at 4.0%. This result currently places the Czech Republic in the position of the European Union’s top performer in the fight against rising prices.

The Structure of February Inflation: What Pushed Prices Lower and What Pushed Them Higher?

- Food as the main brake: Prices in the food and non-alcoholic beverages category rose by only 0.4% year-on-year. The biggest contributors to the easing in overall inflation were a year-on-year decline of 21.3% in oils and fats and 20.4% in semi-skimmed long-life milk. By contrast, beef (+22%) and eggs (+16.5%) remained significantly more expensive than a year ago. Growth in the prices of bakery products and cereals slowed to 1.5%.

- Alcohol and tobacco: The category as a whole rose by 4.0% year-on-year, but the pace of increase is slowing. Tobacco products rose by 5.7% (January: 6.3%), beer by 1.0% (January: 3.3%), and wine by 0.9% (January: 1.4%). On a month-on-month basis, prices in this category actually fell, with wine down 6.2%, beer down 3.5%, and spirits down 3.1%.

- Energy and housing: Electricity prices were 11.9% lower year-on-year and natural gas prices were down 7.2%, still primarily reflecting the January abolition of the renewable energy support surcharge and lower market prices. By contrast, market rents continued to rise, increasing by 6.1% year-on-year.

- Imputed rent: Owner-occupied housing costs continued to rise at a stable pace of 5.1% (the same as in January), reflecting ongoing pressure on new property prices and construction material costs.

- Services under pressure: While goods prices as a whole fell by 0.7% year-on-year, services were 4.5% more expensive. This is particularly visible in catering (+4.2%), accommodation (+6.8%), and social care services (+9.7%).

- Fuel and transport: Fuel prices rose by 1.2% month-on-month in February, reflecting tensions in global oil markets. However, they remained 8.4% lower than a year earlier.

- Recreation and culture: This category saw a year-on-year increase of 5.0%, driven by the start of the season and higher prices for holidays and package tours.

Oil’s Roller-Coaster as a New Risk

An additional risk for the coming months is the development of oil prices. Brent crude surged extraordinarily due to the Iran conflict on Monday, 9 March, briefly climbing to nearly USD 120 per barrel, the highest intraday level since June 2022. Yet already during Monday evening, the price corrected sharply, with Brent falling back to around USD 92 per barrel following signals of possible de-escalation of the conflict in the Middle East. This extreme volatility is also important for inflation: if higher oil and fuel prices were to persist for a longer period, they would gradually feed through into transport, logistics, and broader costs across the economy.

CNB View

The actual inflation reading came in 0.2 percentage points below the CNB’s forecast. Regarding the impact of oil prices. Petr Sklenář, Executive Director of the Monetary Department, explicitly stated:

„Inflation will be affected by an increase in oil prices in the months ahead, but it could still stay below 2%.“

The overall message can be summarized as follows:

„Despite the very favourable developments in headline inflation, elevated core inflation and now also an increase in global cost pressures are reasons for a cautious monetary policy approach.“

Any potential interest rate cut is therefore far from certain.

Impact on Mortgages and Real Estate Investment: This Is Not the End of Inflation, but a Change in Its Structure

For households, the February figure is good news. Low inflation helps stabilize real incomes and inflation expectations. For the rates market and for investors in residential real estate, however, a different signal matters more: the rental and service side of the economy remains significantly above the overall index.

From the perspective of the real estate market, February’s data therefore do not signal that inflation risk has disappeared. Rather, they confirm that its structure is continuing to change. Alongside domestic pressures in services and housing, the risk of imported inflation through energy and high commodity price volatility is returning to the picture.

In this environment, the key factor is not a bet on a rapid decline in interest rates, but asset quality, the ability to maintain occupancy, set rents correctly, and manage operating costs on an ongoing basis. That is precisely why, even in an environment of potentially volatile inflation, it makes sense to focus on residential properties with real cash flow and long-term secured income, rather than on a story built solely on cheaper financing or price appreciation.