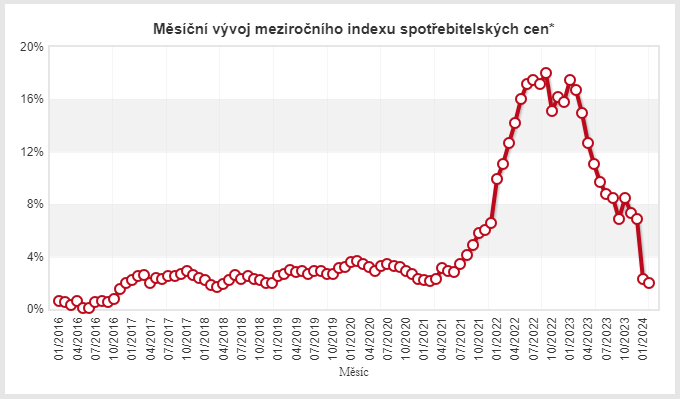

Minulý týden byla oznámena míra inflace v České republice za únor letošního roku. Meziroční míra inflace z lednových 2,3 % klesla na pouhá 2,0 %, což je stejně jako před měsícem nižší než očekávání. Tato míra představuje nejnižší meziroční inflaci od prosince 2018. Důležitým faktorem je skutečnost, že se jedná o cílovou míru inflace České národní banky. Meziměsíční míra inflace činila 0,3 % (očekávání byla 0,4 %).

Bankovní radu potěšil i pokračující pokles jádrové inflace, která se z lednových 2,9 % snížila na únorových 2,8 %. Naopak největším faktorem ve prospěch inflace byly ceny pohonných hmot, které se po několikaměsíčním poklesu vrátily k růstu. Z celkového pohledu byl hlavním faktorem poklesu inflace mimořádně nízký růst ceny zboží o pouhých 0,2 %. Z velké části díky vývoji cen potravin. Proti tomu se ceny služeb (v řadě případů díky inflačním doložkám) zvýšily o 5,2 %.

Inflace v Česku dosáhla sedmé nejnižší hodnoty v Evropské unii. Podle nejnovějších harmonizovaných čísel Eurostatu došlo v únoru k poklesu meziroční míry inflace na 2,2 %, zatímco průměrná míra inflace v Unii klesla z lednových 3,1 % na únorových 2,8 %. V zemích eurozóny klesla z 2,8 % na 2,6 %. Ve všech okolních zemích je inflace vyšší než v České republice – v Německu činí 2,7 %, Polsku 3,7 %, na Slovensku 3,8 % a v Rakousku dokonce 4,2 %.

Petr Král, ředitel sekce měnové politiky ČNB, vyjádřil uznání k neočekávaně nízké inflaci: „Cenová hladina v únoru meziměsíčně vzrostla o 0,3 %. Intenzita tradičního přecenění na počátku roku byla pod předpoklady zimní prognózy. Podle ní se inflace bude v průběhu celého letošního roku pohybovat na dohled 2% cíle.“

V reakci na tento inflační vývoj bankovní rada ČNB snížila 20. března dvoutýdenní repo sazbu o 0,5 % z 6,25 % na většinou analytiků očekávaných 5,75 %, stejně tak i lombardní a diskontní sazbu. Základní úroková sazba je nyní 3,75 procentního bodu nad úrovní inflace. Pro srovnání – ve Spojených státech tento rozdíl činí 2,2 procentního bodu a v eurozóně 1,9 procentního bodu. Bankovní rada má jako jeden z největších jestřábů ještě velkou rezervu pro pokračování ve snižování úrokových sazeb.

Problémem české ekonomiky je minimální růst HDP. Podle Eurostatu ekonomika Evropské unie v posledním čtvrtletí loňského roku ve srovnání se 3. čtvrtletím loňského roku stagnovala. Česko dosáhlo růstu 0,2 %.

V meziročním srovnání ekonomika Evropské unie vzrostla o 0,2 procentního bodu, což představuje zhoršení oproti předchozímu odhadu, který předpokládal růst o 0,3 procenta a česká ekonomika zaznamenala meziroční pokles o 0,2 procentního bodu. I přes oslabení ekonomiky trvá dlouhodobě nízká nezaměstnanost (aktuálně 4,0 %), a to hlavně díky struktuře ekonomiky a odchodům do důchodu.

Celkový rozpočtový deficit v minulém roce dosáhl 3,6 % HDP (pro srovnání – ve Spojených státech činí tento poměr dle St. Louiské pobočky Fedu 6,2 %). Snaha vlády o konsolidaci by měla přispět ke snížení deficitu pod 3 % hranici stanovenou Maastrichtskými kritérii. Snaha o snížení tohoto deficitu vede ke zhoršení vývoje ekonomiky. Míra zadluženosti státu vůči HDP je přitom nízká. Aktuálně činí kolem 45 %, čímž s velkou rezervou splňuje Maastrichtská kritéria pro přijetí eura, kde tento limit činí 60 % a navíc není dodržen většinou zemí eurozóny.

Ohledně letošního vývoje Ministerstvo financí ve své prognóze zveřejněné na konci ledna uvedlo, že v letošním roce očekává růst ekonomiky o 1,2 %, a to především díky obnovenému růstu spotřeby domácností, zvýšení soukromých investic a zvýšení exportu, kterému pomůže i uklidnění situace v dodavatelských řetězcích. V tomto případě se ve srovnání s listopadovou prognózou jedná o významný pokles o 1,9 %. Česká národní banka ve své únorové prognóze snížila očekávaný růst HDP v letošním roce z podzimních 1,2 % na 0,6 % a je tedy větším pesimistou než Ministerstvo financí.

Zde se projevuje problém závislosti české ekonomiky na německé. Podle necelé dva týdny staré prognózy německého hospodářského institutu Ifo se letos očekává v Německu růst pouze 0,2% hrubého domácího produktu. Tento odhad je výrazně nižší než předchozí prognóza, která v lednu počítala s růstem o 0,7 procenta. Kombinací slabého vývoje české ekonomiky s německou (která je největší v Evropě) a vzájemné provázanosti obou zemí, hrozí zlevňování zboží. Výsledkem je ovšem slabý vývoj obou ekonomik.

Je zde tedy riziko deflace, minimálně v případě zboží. Na první pohled je pokles inflace dobrou zprávou. Z dlouhodobějšího hlediska však nižší ceny vytváří tlak na ziskové marže firem, které mohou být přinuceny k nepříznivým opatřením jako je snižování počtu zaměstnanců nebo snižování mezd. Druhá možnost je obvykle nepřijatelná, takže společnosti často volí první variantu, což má negativní dopad na celou ekonomiku. Další problém se týká dražších výrobků. Když spotřebitelé vidí, že ceny klesají, mohou odložit plánované větší nákupy (např. auta) s nadějí, že později koupí levněji. Odložení nákupu však může vést ke snížení celkové spotřeby, což má výrazně negativní vliv na ekonomiku. Zvláště v případě České republiky, která je na automobilovém průmyslu závislá.

Vzhledem k vývoji HDP a klesající inflaci by české ekonomice, závislé na exportu, pomohlo mírné dočasné oslabení koruny. Bankovní rada s oslabením nepočítá, naopak se vyjadřuje ve smyslu, že oslabení české koruny může ve svém důsledku dokonce zpomalit či zastavit snižování úrokových sazeb. Oslabení o několik desetihaléřů vůči euru by bankovní rada ještě řešit nemusela. V případě, že by hrozilo oslabení výrazně větší, má ovšem dostatečně velké devizové rezervy v poměru k HDP dosahují přibližně 44 %. Větší poměr má pouze Singapur a Švýcarsko.

Z dlouhodobého pohledu by pro českou ekonomiku bylo lepší rychlejší snížení úrokových sazeb a mírné oslabení české koruny v kombinaci s inflací mezi 2 % až 3 %, tedy v rámci tolerančního pásma ČNB. Obojí by pomohlo české ekonomice a zároveň obnovilo růst cen nemovitostí. Nebyl by tak dramatický jako byl v letech 2020 a 2021, ale z pohledu investora se již dnes jedná o zajímavou investiční příležitost.

Is Deflation a Possibility in the Czech Republic?

Last week, the Czech Statistical Office announced the inflation rate for February of this year. The year-on-year inflation rate declined from 2.3% in January to 2.0%, lower than expected for the second consecutive month. This rate marks the lowest annual inflation rate since December 2018, meeting the Czech National Bank’s target inflation rate. The month-on-month inflation rate was 0.3%, below the anticipated 0.4%.

The Board was content with the continuous drop in core inflation, decreasing from 2.9% in January to 2.8% in February. However, the main driver of inflation was fuel prices, bouncing back after a period of decline. The primary cause of the inflation decline was the slight rise in goods prices at just 0.2%, primarily driven by food prices. Conversely, service prices (largely due to inflation clauses) increased by 5.2%.

Based on Eurostat’s latest harmonized data, the Czech Republic has achieved the seventh lowest inflation rate in the European Union, with the annual rate dropping to 2.2% in February. Furthermore, the average inflation rate in the EU decreased from 3.1% in January to 2.8% in February, while in the euro area countries, it declined from 2.8% to 2.6%. Notably, neighboring countries such as Germany, Poland, Slovakia, and Austria all have higher inflation rates compared to the Czech Republic. Inflation is 2.7% in Germany, 3.7% in Poland, 3.8% in Slovakia, and even 4.2% in Austria.

Petr Král, the Director of the Monetary Policy Department at the CNB, expressed his gratitude for the unexpectedly low inflation. The price level rose by a mere 0.3% on a monthly basis in February. The intensity of price changes at the beginning of the year was below the assumptions made in the winter forecast. As per the forecast, inflation is projected to remain close to the 2% target throughout the entirety of this year.

Responding to the inflationary trends, the CNB Board decided to lower the two-week repos rate from 6.25% to 5.75% on 20 March, in line with the expectations of most analysts. Additionally, they reduced the Lombard and discount rates by 0.50%. Five board members supported the rate cut, while two members voted for a 0.75% reduction. Currently, the base rate is 3.75 percentage points above inflation, which is higher compared to the United States (2.2 percentage points) and the euro area (1.9 percentage points). Despite being the most hawkish, the Bank Board still has a significant margin to continue reducing interest rates, indicating potential further cuts.

The Czech economy is struggling with minimal GDP growth. Eurostat findings indicate that, unlike the third quarter, the EU economy did not show any growth in the final quarter of the previous year. The Czech Republic experienced a growth of 0.2%.

The European Union economy experienced a growth of 0.2 percentage points year-on-year, resulting in a decrease from the initial estimate of 0.3 percentage points. Conversely, the Czech economy saw a contraction of 0.2 percentage points. Despite the economic slowdown, long-term unemployment has stayed low at 4.0%, largely attributed to the economy’s structure and retirements.

The overall budget deficit reached 3.6% of GDP last year (compared to 6.2% in the United States, according to the St. Louis Fed). The government’s ongoing efforts to consolidate its finances are expected to contribute towards reducing the deficit below the 3% threshold set by the Maastricht criteria. However, these efforts to address the deficit have had adverse effects on the economy. On a positive note, the government’s debt-to-GDP ratio is currently low, standing at around 45%. This comfortably satisfies the Maastricht criteria for adopting the euro, which sets a limit of 60% and is not met by most euro-area countries.

In its forecast released at the end of January, the Ministry of Finance projected a 1.2% economic growth for this year, citing increased household consumption, private investment, and exports (which would also be helped by a calming of the situation in supply chains) as key drivers. This represents a substantial decrease of 1.9% compared to the November forecast. On the other hand, the Czech National Bank’s February forecast paints a more pessimistic picture, with a projected GDP growth of 0.6% for the year.

The Czech economy’s reliance on the German economy is evident in this context. Recent forecasts from the Ifo Institute (Leibniz Institute for Economic Research), released less than two weeks ago, indicate a projected growth of only 0.2% in Germany’s gross domestic product for the year. This forecast is significantly lower than the previous estimate of 0.7% growth in January. The interconnectedness of the Czech and German economies, with Germany being the largest in Europe, poses a risk of driving down the prices of goods. Consequently, both economies may experience sluggish development.

There is a potential risk of deflation, particularly in the case of goods. At first glance, the decrease in inflation may seem like positive news. However, in the long run, lower prices can create challenges for companies‘ profit margins, potentially leading to measures such as staff reductions or wage cuts. The latter option is generally not desirable, so companies often choose the former, which negatively impacts the overall economy. Another issue arises with more expensive products. When consumers witness price declines, they may delay planned major purchases (such as cars) in hopes of obtaining them at a lower cost later on. Nevertheless, postponing purchases can result in a decrease in overall consumption, which significantly harms the economy, especially in the case of the Czech Republic, which heavily relies on the automotive industry.

Given the current GDP development and decreasing inflation, a temporary devaluation of the koruna could be advantageous for the export-oriented Czech economy. The Bank Board, however, does not expect a devaluation and suggests that it might hinder interest rate cuts. A minor devaluation against the euro may not require intervention from the Bank Board. In the event of a substantial devaluation, the Czech koruna has significant foreign exchange reserves, equivalent to approximately 44% of the GDP, a ratio higher than most countries except for Singapore and Switzerland.

In the context of long-term prospects, a more rapid reduction in interest rates and a marginal depreciation of the Czech koruna, coupled with an inflation rate between 2% and 3% within the tolerance bands defined by the CNB, would be more beneficial for the Czech economy. These measures would not only assist the economy but also contribute to the recovery of property prices. Although not as significant as the growth witnessed in 2020 and 2021, this situation already presents an appealing investment opportunity from an investor’s perspective.