November data confirm that the mortgage market is closing out the year in solid shape even without further rate cuts. Activity at banks and building societies remains elevated, with the number of new mortgages holding at around 6,700. Since the start of the year, the total volume of new mortgages has reached CZK 293 billion—CZK 84 billion more than in the same period last year.

The market is currently supported by households’ adaptation to higher interest rates, wage growth, and higher average loan amounts.

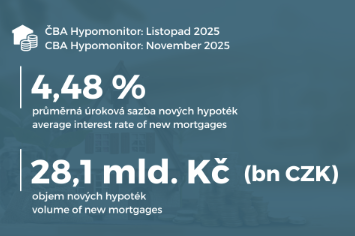

- New mortgages: In November 2025, banks and building societies originated new mortgages totaling CZK 28.1 billion. Compared with October, this represents a slight cooling (-4%); however, after seasonal adjustment, the market has maintained a pace of around CZK 30 billion over the past two months. Hypomonitor also estimates that if the October–November pace is sustained, the volume of new mortgages in 2025 (excluding refinancings) could reach approximately CZK 322 billion.

- Average mortgage interest rate: The average interest rate on new mortgages remained at 4.48%, down 0.37 percentage points year over year.

- Average mortgage size: The average mortgage amount in November reached CZK 4.38 million. The cumulative increase this year is still around CZK 530 thousand (+13.7%). Higher loan amounts, combined with stable rates, help explain why the market continues to post strong figures even without a visible decline in interest rates—and they also support the ongoing rise in property prices.

- Refinancing: Refinancings amounted to CZK 8.9 billion (24% of total volume). Their share has stabilized and reflects maturing fixed-rate periods agreed during the era of low interest rates around the COVID period.

“Mortgage momentum in November remains solid in both volumes and the number of new mortgages, reflecting not only continued growth in property prices but also stronger purchasing power thanks to persistently robust wage growth. If there is no negative shock, we will see higher annual figures not only for 2025,” comments Jaromír Šindel, Chief Economist of the Czech Banking Association.

Global pressures and CNB regulation

A key factor dampening any further decline in mortgage rates in the Czech Republic has been developments in global interest rate markets. Although the U.S. Federal Reserve cut rates for the third time in December, its rhetoric remains cautious, and further easing is far from certain. Without a more pronounced decline in market rates, a significant reduction in Czech mortgage rates is unlikely in the near term.

In the pre-Christmas week, both the European Central Bank (17–18 December) and the Czech National Bank (18 December) will meet; their decisions and commentary will be very important.

It will also be necessary to monitor the new macroprudential recommendation of the Czech National Bank, which will tighten conditions for investment mortgages from April 2026 (affecting roughly 7.5% of loans). According to the Czech Banking Association’s analysis, this measure may slow overall growth in new mortgages next year, especially in higher-priced locations.

Why invest in real estate now

From an investment perspective, it is important that the mortgage market is able to function even with rates around 4.5%—demand has adjusted and remains strong. In an environment of stable rates and rising property prices, regional investment opportunities outside Prague and Brno are gaining in importance, as they offer lower entry costs, higher yields, and better portfolio diversification. Tighter rules for investment mortgages may further reinforce this shift toward the regions.

Salutem Group covers regional markets

Salutem Group, which has long specialized in regional residential real estate, is well-positioned in this environment. We offer investors seeking a combination of stable returns and an accessible entry investment two options:

- Direct investment with a targeted return of up to 6.1% per year.

- Participation through a qualified investors’ fund.

At a time when mortgage rates remain stable below 4.5%, regulation is tightening, and regional markets offer attractive yields, diversifying into regional real estate is a rational choice for investors looking for a combination of stable returns and an accessible entry investment.