Koncept teorie většího hlupáka není doporučovanou investiční strategií. Je krátkodobým finančním přístupem, spojovaným s finančnímu bublinami odtrženými od reality. Investoři ignorují vnitřní hodnotu nebo základy aktiva. Předpokládají, že mohou profitovat z nákupu nadhodnocených aktiv, pokud je mohou prodat jinému investorovi, „většímu hlupákovi“, za ještě vyšší cenu. Ceny aktiv rostou tak dlouho, dokud existují ochotní kupující.

Tyto spekulativní bubliny nakonec splasknou, což vede k rychlému poklesu cen aktiv. Když k tomu dojde, je obtížné najít kupce a investorům (spíše spekulantům), kteří nakoupili za nadsazené ceny, mohou zůstat v držení aktiva, jejichž hodnota je výrazně nižší, než kolik za ně zaplatili.

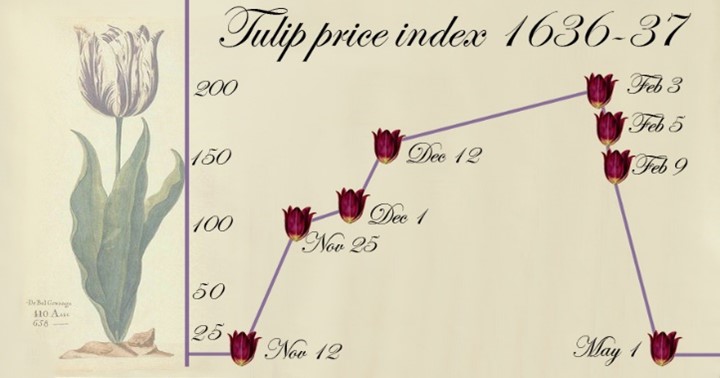

Nejčastěji používaným příkladem jsou holandské tulipány nebo dot-com akcie z konce 90. let minulého století. Zde jsou názorně jejich vývoje.

Prodělečná je pro velkou většinu investorů. Ve své podstatě je zde velké propojení s tzv. Ponziho schématem, ve kterém jsou první investoři placeni penězi od nových investorů, což vytváří cyklus závislosti na hledání dalších a dalších lidí, kteří „investují“.

Investoři provádějící fundamentální analýzu zaměřenou na celkové finanční zdraví společnosti, její výnosy, dividendy či akceptace víceleté prognózy postavené na fundamentech se těchto typů investic či schémat nezúčastňují. Případně okamžitě prodávají, když si všimnou vývoje, který signalizuje začátek takovéhoto schématu.

Typickými kritiky těchto procesu je Warren Buffett a byl jím i Charlie Munger. Pro ně jsou zajímavé pouze akcie firem se silnými a trvalými ekonomickými základy, které jsou schopny v budoucnu generovat značné výnosy v penězích (nejen na papíře).

Nemovitosti však nebyly výjimkou. Na stejném principu je třeba provádět i jejich analýzy. Nelze nakupovat bezhlavě jen proto, že jejich cena minulý měsíc vzrostla, jako se tomu dělo ve Spojených státech několik let před finanční krizí 2008-2009.

Klíčové je pracovat s nemovitostmi jako s dlouhodobými investicemi, nikoli jako s krátkodobými spekulacemi, kdy jsou zakoupeny s úmyslem je brzy prodat, a kupující není ochoten je delší dobu držet. Spolu s tím se nelze se spoléhat na to, že jejich ceny nepřetržitě porostou od nebes. Tak vysoko neporostou.

Proto je pro dlouhodobé investory do nemovitostí velmi důležitý trh s nájemním bydlením. Pozitivem je, že v České republice nevykazuje žádné velké nejasnosti. Díky tomu mají jak nájemníci, tak i pronajímatelé určitou míru jistoty.

Investor však nemůže brát v potaz trh nemovitostí v České republice jako celek, různé oblasti přináší různé výnosy. Například Praha a Brno, které jsou stále pro velkou část investorů jejich jediným lokalitami, které berou v úvahu, se díky tom staly lokalitami s nejnižšími výnosy pod 4% úrovní, spíše ještě níže. A to bez zohlednění časových, administrativních a dalších nákladů. Tento přístup velké skupiny investorů k investicím v Praze nabízí zajímavé investiční příležitosti s vyšším výnosem mimo Prahu. Za pozornost stojí například výnosy v Ústí nad Labem 6,6 %, v Karlových Varech 5,8 % atd.

Důvod rozdílů je jednoduchý. Byt v Praze o ploše 60 m2 stojí 10,4násobek roční průměrné hrubé mzdy v Praze a stejně velký byt v Ústí nad Labem stojí pouze 3,8násobek průměrné hrubé mzdy v Ústeckém kraji a bydlení v Ústí nad Labem zároveň vyjde levněji. Nejen v absolutní částce, ale zároveň i v poměru k příjmům.

Průměrný pronájem bytu Praze zároveň vyjde na 43 procent průměrné měsíční hrubé mzdy v Praze, v Ústí nad Labem je na 27 % průměrné hrubé měsíční mzdy v Ústeckém kraji. Oba tyto rozdíly jsou významné a budou se postupně snižovat, což investoři jistě uvítají.

Navíc nedávné údaje ukazují, že růst nájmů bytů v Praze se zastavil. Za poslední rok a půl došlo k nárůstu o pouhých 5,5 %, což je výrazně méně než inflace, letošní růst z toho je nulový. Tento vývoj naznačuje, že pokud se trend nezmění, příjmy investorů do pražských nemovitostí neporostou.

Tím spíše je v rámci těchto lokalit potřeba detailní analýza každé konkrétní nemovitosti, do které chce investor vložit volné finanční prostředky. Jako vhodná příležitost se investorům nabízí naše nabídka „klíč za klíč“ nabízející investorům řadu výhod. První je zvýšení regionální diverzifikace, druhou zvýšený výnos a třetí je struktura nabídky, ve které nejsou žádné nemovitosti, které neprošly detailní analýzou „due dilligence“ provedou skupinou Salutem Group.

Díky zajištění plné návratnosti vstupní investice se investor nemůže dostat do ztráty a Salutem Group se nikdy neúčastnil a ani se nebude žádného projektu postaveném na konceptu většího hlupáka účastnit.

……..

The Greater Fool Theory

The greater fool theory is not a sound investment strategy to follow. This concept is often utilized in short-term financial maneuvers that are typically linked to financial bubbles that are not based on actual market conditions. Investors who adhere to this theory tend to overlook the true value and fundamentals of an asset, choosing instead to believe that they can make a profit by selling overpriced assets to another investor, known as the „greater fool,“ at a higher price. As long as there are willing buyers in the market, asset prices will continue to escalate.

The bursting of speculative bubbles results in a sudden drop in asset prices. Finding buyers becomes a challenge, and those who buy at inflated prices, typically speculators, may end up with assets that are worth much less than what they originally paid for them.

Dutch tulips and dot-com stocks from the late 1990s are the most frequently utilized examples. Below are depictions of how they have developed over time.

It is unprofitable for the vast majority of investors. Essentially, it bears a strong resemblance to the Ponzi scheme, where initial investors are compensated with funds from new investors, leading to a reliance on continually recruiting new individuals to „invest“.

Investors who perform fundamental analysis focus on the company’s overall financial health, its earnings, dividends, and willingness to accept multi-year forecasts based on fundamentals. They do not engage in these types of investments or schemes. Instead, they promptly sell their holdings when they observe any development that indicates the beginning of such a scheme.

Warren Buffett and Charlie Munger are common critics of such procedures. They are solely interested in stocks of companies with robust and long-lasting economic fundamentals that can produce substantial cash returns in the future, rather than just on paper.

Real estate, nevertheless, was not excluded. Their analysis should be conducted on the same principle. One should not purchase haphazardly just because their price rose last month, as was the case in the United States for several years before the 2008-2009 financial crisis.

The crucial strategy is to view real estate as a long-term investment, rather than a short-term gamble aimed at immediate resale. Investors must be willing to retain ownership for an extended duration, as prices do not always escalate significantly.

For long-term real estate investors, the rental housing market plays a crucial role. The Czech Republic’s stable conditions provide a sense of security for both tenants and landlords.

However, it is essential for an investor to acknowledge that the real estate market in the Czech Republic is not homogeneous, resulting in different investment returns across various areas. For example, Prague and Brno, which have historically been the main focus for investors, now offer the lowest yields at less than 4%, or even lower. This does not even consider the time, administrative, and other associated costs. Consequently, the prevailing investment strategy in Prague presents attractive opportunities for higher yields in locations outside the capital, such as Ústí nad Labem with a yield of 6.6%, and Karlovy Vary with a yield of 5.8%.

The cause of the distinctions is clear. A 60 m2 apartment in Prague is valued at 10.4 times the annual average gross wage in Prague, whereas an apartment of the same size in Ústí nad Labem costs only 3.8 times the average gross wage in the Ústí nad Labem region, highlighting the affordability of living in Ústí nad Labem, not just in absolute terms but also concerning income.

At the same time, the average rent for an apartment in Prague represents 43% of the average gross monthly wage in Prague, while in Ústí nad Labem, it constitutes 27% of the average gross monthly wage in the Ústí nad Labem region. These discrepancies are significant and are forecast to diminish progressively, a development that is likely to be positively received by investors.

Furthermore, recent data reveals that the escalation of apartment rents in Prague has ceased. In the last year and a half, there has been a mere 5.5% increase, which is considerably lower than the inflation rate, and there has been no growth this year. This trend indicates that, unless there is a change, the returns from investing in Prague real estate will not increase.

A comprehensive examination of each specific property that an investor wishes to allocate their free funds to is crucial. Our turnkey offer presents an attractive opportunity for investors, offering a range of advantages. Firstly, it provides increased regional diversification. Secondly, it offers a higher yield. Lastly, the offer is structured to exclude any properties that have not undergone a thorough „due diligence“ analysis by Salutem Group.

By ensuring a full return on the initial investment, the investor is shielded from any potential losses. Salutem Group has never engaged in, and will never engage in, any project that is based on the greater fool concept.